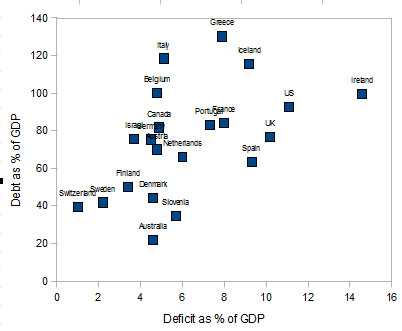

look at portugal and england

which one is in the tit twister now

long live the euro zone

iron maiden of piig misery

The government doesn't need to add jobs, per se, the government needs to figure out how to get corporate America to drop the saving glut and re-invest in the economy."

The government doesn't need to add jobs, per se, the government needs to figure out how to get corporate America to drop the saving glut and re-invest in the economy."

" The study shows that currency appreciations can help to a certain extent in reducing global imbalances, and that it can go along with a shift from a mainly export-based model of growth towards a model with internal sources of growth. The cost in terms of growth would be very limited in the case of developed countries, but somewhat larger for developing countries.

Using data for 128 countries between 1960 and 2008, we have found 25 episodes of large sustained exchange rate revaluations, which we define as both nominal and real effective exchange rate appreciations of 10% (and more) within a two year window (or less). Studying the institutional context of each individual episode in detail, we identified 14 cases of appreciation shocks that occurred not as a result of discretionary policy action, but were passively linked to the appreciation of the anchor currency in the context of an exchange rate peg. We argue that these cases represent instances of exogenous appreciation shocks that we can use to estimate the macroeconomic impact of large appreciations and assess the robustness of estimates based on a wider definition of appreciation and revaluation events. Using a dummy-augmented autoregressive panel model we could indeed show that such large appreciations episodes have strong macroeconomic effects. Most importantly, we established four key stylised facts that can prove useful in the ongoing debate about the role of exchange rate adjustment for global rebalancing.It is interesting to consider these results in the context of other studies. In particular, Eichengreen and Rose (2010) conducted an study of "...what happens to economies when they exit exchange rate pegs that are resisting appreciation. Data from 27 cases suggest that growth slows but only modestly, and there is no evidence of economic and financial damage as a result -- certainly nothing like the fears that China's next decade could look like Japan's lost decade." [pdf].

First, the current account balance typically falls strongly in response to large exchange rate revaluations. Three years after the revaluation, the current account balance deteriorates by about 3 pp. relative to GDP. This is due to a reduction in aggregate savings without a concomitant fall in investment. The effect on the current account balance is statistically significant and robust to variation in the country sample and the definition of appreciation events.

Second, the effects on output seem limited. Our point estimates suggest a negative effect of output growth, albeit of relatively small magnitude: on average, the aggregate level effect on output amounts to about 1% after six years. The confidence intervals are also considerably wider than for the current account. The output effects are statistically not significant.

Third, while aggregate output is not strongly affected, export growth falls significantly after appreciation shocks. Import growth remains by and large unchanged resulting in the observed deterioration in external balances. As aggregate economic growth is much less affected, our results point to a positive domestic demand response following appreciation episodes.

Fourth, these effects seem to be more pronounced in developing countries. The sensitivity of the current account balance to revaluation shocks is higher. The effect reaches almost 4 percentage points of GDP after three years and is statistically significant. But also the potentially negative effects on output are larger. Our point estimates indicate a loss in output of 2% over ten years. But confidence intervals remain wide, so that these results miss statistically significant levels. Why these effects are stronger in developing countries will be an important question that we aim to address in future research.

In sum, the historical record of large exchange rate revaluations that we have studied in this paper lends some support to the idea that large exchange rate appreciations and revaluations have an impact on the current account as they lead to marked changes of savings and investment within countries. Appreciation shocks impact external balances, but this effect potentially comes at the cost of a reduction of dynamism in exports. While the domestic economy seems to pick up some of the external slack, leaving overall growth relatively unaffected, the prospect of sharp decelerations in export growth will remain a concern for policy-makers and bears watching especially in the context of developing countries.

Bureau of Labor Statistics, via Haver Analytics

Bureau of Labor Statistics, via Haver Analytics

{kind=link}

simple message drink that booze like you drink it now

for another 15 years and you'll have a pink elephant moment

and a 5 year turkey trot over thin ice

but cut that crap out now

sure the joy of the happy hour high will leave its cavity in the soul of your job day

but

a certain purgatory trumps a perfect hell baby

pure preacher boy bull balls