pretty hard here

in particular the neutrality assumption NA

" •Why the Pigou Effect does not get you out of a liquidity trap - mainly macro "

NA is yet another of many attempts to smuggle in the class consequences of pareto neutrality

here its infinite horizon

inter temporal government budget balancing

yes as a iron rule of government action

okay in the base line model

where

the balance occurs over the infinite horizon

and is

faced by an infinite lived single rep agent

but

sustained within the fairly short run horizon

of real taxpayers and debt holders

which may possibly mean

within two cycle

this neutrality

this rebalancing looks onerous

and lopsidedly stacked against

adequate counter cyclical state fiscal action

an excessive build up of nominal state obligations

--even or should I say in particular fully monetized--

to fund recovery rate enhancing state to citizen pay outs

to meet the pledged neutrality

leads to a full off set

thru an expected inflation tax

answer

Pareto constraints are bunk

ie requiring that

everyone after implementing a policy program

ends up at least as well off as without said program

is a formula that favors the have class the exploiter class the corporate class in our set up

over the job class

class struggle is non Pareto optimal at all times

in other words

social reality in a class cloven society

is inherently non Pareto optimal

the neutral state favors the private exploiters

Thursday, August 15, 2013 at 07:51 AM

paine said in reply to paine ...

mealy macro here

using the classic narrow definition

of the pigou effect

is btw

not generalizing his thesis

to cover the various QE channels

beloved of our ski mobiler

using the classic narrow definition

of the pigou effect

is btw

not generalizing his thesis

to cover the various QE channels

beloved of our ski mobiler

paine said in reply to paine ...

once again

as when on one the duke of toon town

old nick rowe's

microscopic stick figure

geek-o-nomical diversions

think of legal tender money as just

uncle sam issued

zero coupon consoles

as when on one the duke of toon town

old nick rowe's

microscopic stick figure

geek-o-nomical diversions

think of legal tender money as just

uncle sam issued

zero coupon consoles

paine said in reply to paine ...

the console has no obligatory redemption

removing the formal basis for

inter temporal budget neutrality

----------------------------------------------------------

removing the formal basis for

inter temporal budget neutrality

----------------------------------------------------------

bakho said...

The inflation everyone worries about is the wage-price spiral. This is kept in check by policy to suppress wages. IOW, the Fed creates a mild recession to put people out of work and take out upward pressure on wages.

In an economy with 7 percent unemployment and a global supply of cheap labor, there is No domestic wage inflation. No monetary policy will create domestic wage inflation. Domestic wage inflation can only arise if labor has strong bargaining positions. This demands that the economy be at full employment. Then the wages of domestic labor can be bid up, but not until then.

Wages will inflate only if Congress raises min wage or if labor is in a strong enough position to bargain upward the wages of the employed. When is the last time labor showed an ability to bargain up wages for large numbers of American workers? We have had "temporary wage inflation" with some of the tax cuts for workers and transfer payments. However, those are gone.

The Friedman focus on monetary policy left out the very important mechanisms that set and inflate wages.

In an economy with 7 percent unemployment and a global supply of cheap labor, there is No domestic wage inflation. No monetary policy will create domestic wage inflation. Domestic wage inflation can only arise if labor has strong bargaining positions. This demands that the economy be at full employment. Then the wages of domestic labor can be bid up, but not until then.

Wages will inflate only if Congress raises min wage or if labor is in a strong enough position to bargain upward the wages of the employed. When is the last time labor showed an ability to bargain up wages for large numbers of American workers? We have had "temporary wage inflation" with some of the tax cuts for workers and transfer payments. However, those are gone.

The Friedman focus on monetary policy left out the very important mechanisms that set and inflate wages.

samuel said in reply to bakho...

Bakho

I agree. Do all these economists need to lose their jobs and then have to go out and find new jobs at current wages to figure this out?

I agree. Do all these economists need to lose their jobs and then have to go out and find new jobs at current wages to figure this out?

Mark A. Sadowski said in reply to bakho...

"In an economy with 7 percent unemployment and a global supply of cheap labor, there is No domestic wage inflation. No monetary policy will create domestic wage inflation. Domestic wage inflation can only arise if labor has strong bargaining positions. This demands that the economy be at full employment. Then the wages of domestic labor can be bid up, but not until then.

Wages will inflate only if Congress raises min wage or if labor is in a strong enough position to bargain upward the wages of the employed. When is the last time labor showed an ability to bargain up wages for large numbers of American workers? We have had "temporary wage inflation" with some of the tax cuts for workers and transfer payments."

First of all the labor share of income has been falling everywhere (advanced, emerging and developing) for over 20 years so globalization is unlikely to be the problem.

When did we last have tight labor markets and wage inflation generated by those markets? In 1997-2001.

Here's the unemployment rate versus the natural rate of unemployment from 1993-2005:

http://research.stlouisfed.org/fred2/graph/?graph_id=133007&category_id=0

This caused real hourly and weekly earnings to increase significantly:

http://research.stlouisfed.org/fred2/graph/?graph_id=133008&category_id=0

(Note that there was a shift upward because of the recession but that is normal and is more due to the layoff of low earning employees and not an improvement in real earnings.)

The labor share of factor income surged and this was followed by an increase in core inflation:

http://research.stlouisfed.org/fred2/graph/?graph_id=133009&category_id=0

Did minimum wages or unions play a role?

Minimum wages were increased from $4.25 an hour in 1996 to $5.15 an hour in 1998. As a percent of average hourly earnings they increased from 36.5% in 1996 to 39.6% in 1998 but they fell back down to 35.4% by 2001, so that is unlikely.

http://www.dol.gov/whd/minwage/chart.htm

The unionization rate of wage and salary workers was 14.0% in 1996 and fell to 12.9% in 2001 (Appendix A, table A1):

http://digitalcommons.ilr.cornell.edu/cgi/viewcontent.cgi?article=1176&context=key_workplace

So it would seem to have been the tighter labor markets and not labor market institutions that brought this about.

Did fiscal policy contribute?

The cyclically adjusted budget balance increased from (-0.8%) of potential GDP in FY 1996 to 1.2% in FY 2000:

http://www.cbo.gov/sites/default/files/cbofiles/attachments/43977_AutomaticStablilizers3-2013.pdf

This was later cut to 0.6% in FY 2001 largely because of the first phase of Bush's tax cuts. But this was too small and too late to explain the increase in aggregate demand that occured in the late 1990s.

So the 1997-2001 wage boom was largely caused by expansionary monetary policy.

Wages will inflate only if Congress raises min wage or if labor is in a strong enough position to bargain upward the wages of the employed. When is the last time labor showed an ability to bargain up wages for large numbers of American workers? We have had "temporary wage inflation" with some of the tax cuts for workers and transfer payments."

First of all the labor share of income has been falling everywhere (advanced, emerging and developing) for over 20 years so globalization is unlikely to be the problem.

When did we last have tight labor markets and wage inflation generated by those markets? In 1997-2001.

Here's the unemployment rate versus the natural rate of unemployment from 1993-2005:

http://research.stlouisfed.org/fred2/graph/?graph_id=133007&category_id=0

This caused real hourly and weekly earnings to increase significantly:

http://research.stlouisfed.org/fred2/graph/?graph_id=133008&category_id=0

(Note that there was a shift upward because of the recession but that is normal and is more due to the layoff of low earning employees and not an improvement in real earnings.)

The labor share of factor income surged and this was followed by an increase in core inflation:

http://research.stlouisfed.org/fred2/graph/?graph_id=133009&category_id=0

Did minimum wages or unions play a role?

Minimum wages were increased from $4.25 an hour in 1996 to $5.15 an hour in 1998. As a percent of average hourly earnings they increased from 36.5% in 1996 to 39.6% in 1998 but they fell back down to 35.4% by 2001, so that is unlikely.

http://www.dol.gov/whd/minwage/chart.htm

The unionization rate of wage and salary workers was 14.0% in 1996 and fell to 12.9% in 2001 (Appendix A, table A1):

http://digitalcommons.ilr.cornell.edu/cgi/viewcontent.cgi?article=1176&context=key_workplace

So it would seem to have been the tighter labor markets and not labor market institutions that brought this about.

Did fiscal policy contribute?

The cyclically adjusted budget balance increased from (-0.8%) of potential GDP in FY 1996 to 1.2% in FY 2000:

http://www.cbo.gov/sites/default/files/cbofiles/attachments/43977_AutomaticStablilizers3-2013.pdf

This was later cut to 0.6% in FY 2001 largely because of the first phase of Bush's tax cuts. But this was too small and too late to explain the increase in aggregate demand that occured in the late 1990s.

So the 1997-2001 wage boom was largely caused by expansionary monetary policy.

Tom Shillock said in reply to Mark A. Sadowski...

"First of all the labor share of income has been falling everywhere (advanced, emerging and developing) for over 20 years so globalization is unlikely to be the problem."

That is when the USSR imploded and workers in Asia began to enter the global workforce in a major way. See the work of Richard Freeman, labor economist at Harvard.

That is when the USSR imploded and workers in Asia began to enter the global workforce in a major way. See the work of Richard Freeman, labor economist at Harvard.

Paine said in reply to Tom Shillock...

Mark ski

Has no truck with global effects only a set of national snap shots

If these various time tagged snap shots

look synchronized in some dimension or other

Like falling wage share that must be about synchronized

National monetary policies

No way could

Growing cross border profit arbitrage

In a world economy segmented into localized price markets and wage pools

increase the share of each nations corporate earnings

in total national income

It's not globalization

look else where friend

Look to the nominal dynamics and the yield curve

Has no truck with global effects only a set of national snap shots

If these various time tagged snap shots

look synchronized in some dimension or other

Like falling wage share that must be about synchronized

National monetary policies

No way could

Growing cross border profit arbitrage

In a world economy segmented into localized price markets and wage pools

increase the share of each nations corporate earnings

in total national income

It's not globalization

look else where friend

Look to the nominal dynamics and the yield curve

Mark A. Sadowski said in reply to Tom Shillock...

I think you may miss my point.

Freeman's hypothesis is that an enlargement of the "global" workforce may explain why the labor share of income in OECD nations is falling. But this does not explain why the labor share of income is falling in the BRIC countries and other emerging and developing economies as well.

Furthermore the downward trend in labor share of income in the advanced world dates all the way back to the 1970s. The downward trend in the emerging and developing economies may date back further than 20 years but we do not have very good data.

Moreover econometric evidence does not support the hypothesis that globalization is responsible for declining labor share:

Effects of Globalization on Labor’s Share in National Income

Anastasia Guscina

December 2006

Abstract:

"The past two decades have seen a decline in labor’s share of national income in several industrial countries. This paper analyzes the role of three factors in explaining movements in labor’s share––factor-biased technological progress, openness to trade, and changes in employment protection––using a panel of 18 industrial countries over 1960–2000. Since most studies suggest that globalization and rapid technological progress (associated with accelerated information technology development) began in the mid-1980s, the sample is split in 1985 into preglobalization/pre-IT revolution and postglobalization/post-IT revolution eras. The results suggest that the decline in labor’s share during the past few decades in the OECD member countries may have been largely an equilibrium, rather than a cyclical, phenomenon, as the distribution of national income between labor and capital adjusted to capital-augmenting technological progress and a more globalized world economy."

http://www.imf.org/external/pubs/ft/wp/2006/wp06294.pdf

The results on page 20 (Table A2.1) are relevant. Trade openness has a significant positive effect on the level (but not rate of change) of labor share of income pre-1985 and a significant negative effect on the level of labor share of income post-1985. More importantly is the effect of trade with developing countries, which is significantly positive in levels pre-1985 and positive although insignificant post-1985.

Freeman's hypothesis is that an enlargement of the "global" workforce may explain why the labor share of income in OECD nations is falling. But this does not explain why the labor share of income is falling in the BRIC countries and other emerging and developing economies as well.

Furthermore the downward trend in labor share of income in the advanced world dates all the way back to the 1970s. The downward trend in the emerging and developing economies may date back further than 20 years but we do not have very good data.

Moreover econometric evidence does not support the hypothesis that globalization is responsible for declining labor share:

Effects of Globalization on Labor’s Share in National Income

Anastasia Guscina

December 2006

Abstract:

"The past two decades have seen a decline in labor’s share of national income in several industrial countries. This paper analyzes the role of three factors in explaining movements in labor’s share––factor-biased technological progress, openness to trade, and changes in employment protection––using a panel of 18 industrial countries over 1960–2000. Since most studies suggest that globalization and rapid technological progress (associated with accelerated information technology development) began in the mid-1980s, the sample is split in 1985 into preglobalization/pre-IT revolution and postglobalization/post-IT revolution eras. The results suggest that the decline in labor’s share during the past few decades in the OECD member countries may have been largely an equilibrium, rather than a cyclical, phenomenon, as the distribution of national income between labor and capital adjusted to capital-augmenting technological progress and a more globalized world economy."

http://www.imf.org/external/pubs/ft/wp/2006/wp06294.pdf

The results on page 20 (Table A2.1) are relevant. Trade openness has a significant positive effect on the level (but not rate of change) of labor share of income pre-1985 and a significant negative effect on the level of labor share of income post-1985. More importantly is the effect of trade with developing countries, which is significantly positive in levels pre-1985 and positive although insignificant post-1985.

bakho said in reply to Mark A. Sadowski...

You confuse correlation with cause and effect.

Tight labor domestic labor markets and highest in a long time employment rates indicated a tight domestic labor market. The tight market caused employers to bid up wages. Money supply was much more expansionary post 9/11 and post fiscal crisis without causing wages to boom. So expansionary monetary policy, by itself is not sufficient to cause wages to increase.

Tight labor domestic labor markets and highest in a long time employment rates indicated a tight domestic labor market. The tight market caused employers to bid up wages. Money supply was much more expansionary post 9/11 and post fiscal crisis without causing wages to boom. So expansionary monetary policy, by itself is not sufficient to cause wages to increase.

Paine said in reply to bakho...

For mark correlation is cause

That is once you sort true an incomplete distorted list of alternatives

Till only your nominated driver remains

Yes it's shooting fish in a barrel

Choose carefully five possible causes

asset they exhaust the possible suspects

One by one eliminate 4 for lack of correlation or whatever else looks black and white

Possible impact Size ...mechanism plausibility whatever

Now presto

The fifth must be

The cause

That is once you sort true an incomplete distorted list of alternatives

Till only your nominated driver remains

Yes it's shooting fish in a barrel

Choose carefully five possible causes

asset they exhaust the possible suspects

One by one eliminate 4 for lack of correlation or whatever else looks black and white

Possible impact Size ...mechanism plausibility whatever

Now presto

The fifth must be

The cause

Mark A. Sadowski said in reply to bakho...

"Tight labor domestic labor markets and highest in a long time employment rates indicated a tight domestic labor market. The tight market caused employers to bid up wages."

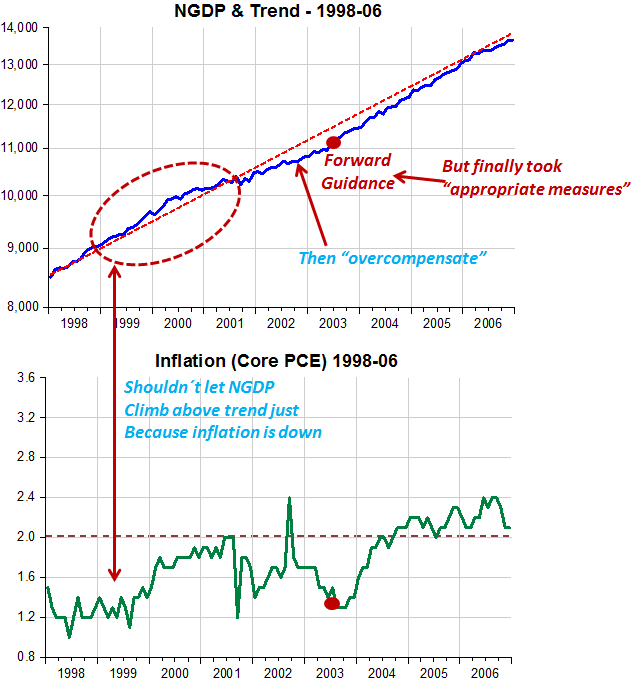

That's my whole point. But what causes tight labor markets? Sufficient aggregate demand, which by definition is simply nominal GDP (NGDP).

"Money supply was much more expansionary post 9/11 and post fiscal crisis without causing wages to boom. So expansionary monetary policy, by itself is not sufficient to cause wages to increase."

There are two ways policymakers can increase NGDP: fiscal and monetary policy. Fiscal policy became very expansionary in FY 2001-2004 thanks to the Bush tax cuts with the cyclically adjusted budget balance falling from 1.2% of potential GDP in 2000 to (-3.2%) of potential GDP in 2004 (see CBO link above).

The velocity of money is unstable so judging monetary policy stance by it is questionable. However if we look at the year on year changes of MZM you will note a big increase in the rate of change in MZM from April 1995 to February 1999 which corresponds to the late 1990s wage boom:

http://research.stlouisfed.org/fred2/graph/?graph_id=133033&category_id=0

There was another surge during 2001 but that coincided with a decline in velocity when the Fed was trying to counteract the recession. Note also that the rate of change in MZM fell steadily from early 2002 through late 2004 during the "jobloss" recovery.

More important is how NGDP behaved during this time period:

http://thefaintofheart.files.wordpress.com/2013/08/doomsayers_2.png

Note that NGDP was above trend in the late 1990s and below trend in the early 2000s. Put it alltogether and what you have is loose monetary policy coupled with tight fiscal policy in the late 1990s during the wage boom and tight monetary policy coupled with loose fiscal policy during the jobloss recovery.

That's my whole point. But what causes tight labor markets? Sufficient aggregate demand, which by definition is simply nominal GDP (NGDP).

"Money supply was much more expansionary post 9/11 and post fiscal crisis without causing wages to boom. So expansionary monetary policy, by itself is not sufficient to cause wages to increase."

There are two ways policymakers can increase NGDP: fiscal and monetary policy. Fiscal policy became very expansionary in FY 2001-2004 thanks to the Bush tax cuts with the cyclically adjusted budget balance falling from 1.2% of potential GDP in 2000 to (-3.2%) of potential GDP in 2004 (see CBO link above).

The velocity of money is unstable so judging monetary policy stance by it is questionable. However if we look at the year on year changes of MZM you will note a big increase in the rate of change in MZM from April 1995 to February 1999 which corresponds to the late 1990s wage boom:

http://research.stlouisfed.org/fred2/graph/?graph_id=133033&category_id=0

There was another surge during 2001 but that coincided with a decline in velocity when the Fed was trying to counteract the recession. Note also that the rate of change in MZM fell steadily from early 2002 through late 2004 during the "jobloss" recovery.

More important is how NGDP behaved during this time period:

http://thefaintofheart.files.wordpress.com/2013/08/doomsayers_2.png

{kind=link}

Note that NGDP was above trend in the late 1990s and below trend in the early 2000s. Put it alltogether and what you have is loose monetary policy coupled with tight fiscal policy in the late 1990s during the wage boom and tight monetary policy coupled with loose fiscal policy during the jobloss recovery.

Rune Lagman said in reply to Mark A. Sadowski...

"Sufficient aggregate demand, which by definition is simply nominal GDP (NGDP)."

NGDP-targeting, in this context, is monetarist-speak for, across-the-board, higher wages. Higher inflation expectations are supposed to induce workers to demand wages that keep up with inflation.

It might work in Europe, where unions are ever-present and relatively strong. Here, in the US, the average, non-union, American lack the market power to keep up with the higher inflation expectations. Current US policy is to prevent inflation by depressing wages.

You and Bakho are, more or less, saying the same thing: "higher wages is the solution".

Bakho just don't believe that higher inflation expectations (NGDP-targeting) will get us there.

I concur with Bakho. I believe, that fiscal policy is the only thing that will goose US labor market, sufficiently, to cause higher wages.

NGDP-targeting, in this context, is monetarist-speak for, across-the-board, higher wages. Higher inflation expectations are supposed to induce workers to demand wages that keep up with inflation.

It might work in Europe, where unions are ever-present and relatively strong. Here, in the US, the average, non-union, American lack the market power to keep up with the higher inflation expectations. Current US policy is to prevent inflation by depressing wages.

You and Bakho are, more or less, saying the same thing: "higher wages is the solution".

Bakho just don't believe that higher inflation expectations (NGDP-targeting) will get us there.

I concur with Bakho. I believe, that fiscal policy is the only thing that will goose US labor market, sufficiently, to cause higher wages.

Mark A. Sadowski said in reply to Rune Lagman...

NGDP targeting will stabilize the level of NGDP which in turn will stabilize the (growing) level of real wages. It only promises to eliminate aggregate demand deficiencies, not necessarily to permanently increase labor share.

The biggest problem with the theory that the decline of unions are responsible for the decline in the labor share of national income is that the decline in labor share of national income was essentially universal throughout the advanced world, and yet union coverage rates have not declined everywhere. See Figure 10 on page 14:

http://www.cepr.net/documents/publications/unions-oecd-2011-11.pdf

Note that union coverage rates increased from 1980 to 2007 in Finland, France, Norway, Spain and Sweden and if you look at the table I posted below the labor share of income declined by 10.8 to 18.3 points in those countries. In fact I've regressed the change in labor income share for these same 18 OECD members against the change in union coverage rates, and the R-squared value is 0.0038 meaning that only 0.38% of the change in labor share of national income can be explained by the change in union coverage rates.

This is not to say that union coverage rates aren't an important factor in explaining changes in the *distribution of labor income*. It's just that they don't match up the data on changes in *labor share of ntional income* very well.

For example the peak year for unionization in the US was 1954 when 33.8% of all wage and salary workers were in a union (see Table A-1):

http://digitalcommons.ilr.cornell.edu/cgi/viewcontent.cgi?article=1176&context=key_workplace

At that time the labor share of National Income was only 61.8%. By the time labor share of National Income peaked at 67.7% in 1980 union membership had already declined to 22.3%. By 2003 union membership had dropped to 12.4% and yet the labor share of National Income in 2011 was 62.1%, or higher than when union membership was at its peak.

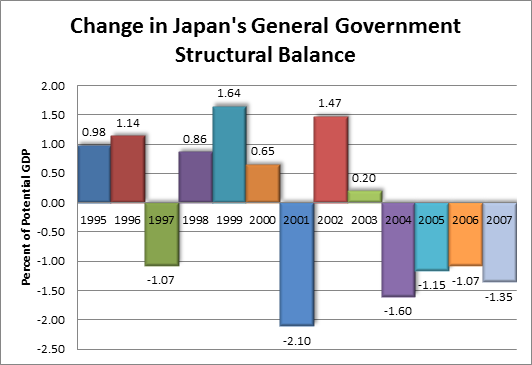

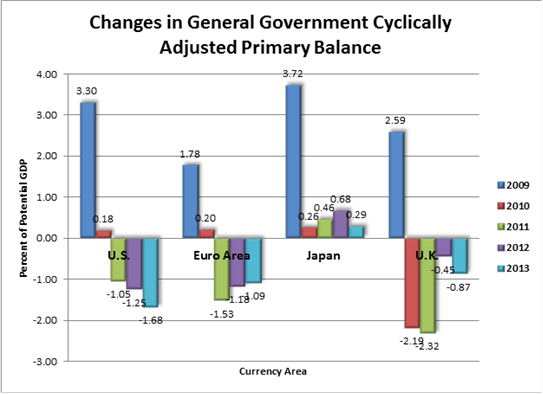

I am as skeptical of fiscal stimulus as you are of monetary policy. Fiscal stimulus only works through changes in the cyclically adjusted budget balance. Thus it's theoretically impossible to maintain positive fiscal stimulus forever. If anyone has any doubts about the practical effectiveness of fiscal stimulus you have only to look at Japan where with the exception of 1997, 2001, and 2004-07 they have had expansionary fiscal policy for over two decades:

http://thefaintofheart.files.wordpress.com/2013/06/sadowski2b_4.png

http://thefaintofheart.files.wordpress.com/2013/06/sadowski3_10.png

And yet nominal GDP is lower now than it was in 1994.

That's why the Japanese now have Abenomics, which despite all the misperceptions in the West, is really about combining monetary stimulus with fiscal austerity (the doubling of the consumption tax from 5% to 10%).

The biggest problem with the theory that the decline of unions are responsible for the decline in the labor share of national income is that the decline in labor share of national income was essentially universal throughout the advanced world, and yet union coverage rates have not declined everywhere. See Figure 10 on page 14:

http://www.cepr.net/documents/publications/unions-oecd-2011-11.pdf

Note that union coverage rates increased from 1980 to 2007 in Finland, France, Norway, Spain and Sweden and if you look at the table I posted below the labor share of income declined by 10.8 to 18.3 points in those countries. In fact I've regressed the change in labor income share for these same 18 OECD members against the change in union coverage rates, and the R-squared value is 0.0038 meaning that only 0.38% of the change in labor share of national income can be explained by the change in union coverage rates.

This is not to say that union coverage rates aren't an important factor in explaining changes in the *distribution of labor income*. It's just that they don't match up the data on changes in *labor share of ntional income* very well.

For example the peak year for unionization in the US was 1954 when 33.8% of all wage and salary workers were in a union (see Table A-1):

http://digitalcommons.ilr.cornell.edu/cgi/viewcontent.cgi?article=1176&context=key_workplace

At that time the labor share of National Income was only 61.8%. By the time labor share of National Income peaked at 67.7% in 1980 union membership had already declined to 22.3%. By 2003 union membership had dropped to 12.4% and yet the labor share of National Income in 2011 was 62.1%, or higher than when union membership was at its peak.

I am as skeptical of fiscal stimulus as you are of monetary policy. Fiscal stimulus only works through changes in the cyclically adjusted budget balance. Thus it's theoretically impossible to maintain positive fiscal stimulus forever. If anyone has any doubts about the practical effectiveness of fiscal stimulus you have only to look at Japan where with the exception of 1997, 2001, and 2004-07 they have had expansionary fiscal policy for over two decades:

http://thefaintofheart.files.wordpress.com/2013/06/sadowski2b_4.png

{kind=link}

http://thefaintofheart.files.wordpress.com/2013/06/sadowski3_10.png

{kind=link}

And yet nominal GDP is lower now than it was in 1994.

That's why the Japanese now have Abenomics, which despite all the misperceptions in the West, is really about combining monetary stimulus with fiscal austerity (the doubling of the consumption tax from 5% to 10%).

Paine said in reply to Mark A. Sadowski...

Your narrative is

Often Brittle

at turns pedantic and obvious

And it ends with a tautology ..for u

Of course it was

expansionary monetary policy

behind that graceful wage boom

For you there is no way past tight money to a phase of greater prosperity

Corporate and household spending are ever and always thrall to monetary policy

One might call it an unreal business cycle theory

Often Brittle

at turns pedantic and obvious

And it ends with a tautology ..for u

Of course it was

expansionary monetary policy

behind that graceful wage boom

For you there is no way past tight money to a phase of greater prosperity

Corporate and household spending are ever and always thrall to monetary policy

One might call it an unreal business cycle theory

The real problem

Mark ski thinks economics is about discovery the workings of a machine

When economics is fundamentally a historical science

All we have in his above narrative is one interval

And one proximate cause

A tighter job market

What in that instance ..the clinton miracle

...produced and sustained that tighter job market

Is specific to that interval

Fortunately if we know a few different ways to tighten job markets

And we do

--- hell Even mark ski knows many of them---

We can just set our goal and start an FDR like pragmatic scramble till we get there

chit chat about a natural rate of anything

Of course

Only helps retard an eclectic process of discovery

And fantasy panaceas deliverable by a fed

following a simple rule

Is bound to end in shambles even as it may be cheered as masterful

Both bens immediate priors had long lines of cheering nit wits

Both were monstrously indifferent to job class welfare

One butchered his way to wall streets notion of a brighter future

The other was that brighter future

And then came fall 08

Mark ski thinks economics is about discovery the workings of a machine

When economics is fundamentally a historical science

All we have in his above narrative is one interval

And one proximate cause

A tighter job market

What in that instance ..the clinton miracle

...produced and sustained that tighter job market

Is specific to that interval

Fortunately if we know a few different ways to tighten job markets

And we do

--- hell Even mark ski knows many of them---

We can just set our goal and start an FDR like pragmatic scramble till we get there

chit chat about a natural rate of anything

Of course

Only helps retard an eclectic process of discovery

And fantasy panaceas deliverable by a fed

following a simple rule

Is bound to end in shambles even as it may be cheered as masterful

Both bens immediate priors had long lines of cheering nit wits

Both were monstrously indifferent to job class welfare

One butchered his way to wall streets notion of a brighter future

The other was that brighter future

And then came fall 08

Ah yes fall 08

Ben's time to shine

Ben's time to shine

Mark A. Sadowski said in reply to bakho...

Michael Kalecki was probably the first to propose a theory of the aggregate income distribution hinging on the determinants of firms’ market power. In particular:

(1938): ”The Determinants of the Distribution of National Income”, Econometrica, 6, 97-112.

(1954): Theory of Economic Dynamics, George Allen and Unwin, London.

The literature on price determination shows that firms’ markups depend on factors like industry concentration, collusion, demand elasticity, and the potential entry of other firms into a market. Most changes in these variables are uncorrelated across industries. Nonetheless, they are simultaneously affected by the business cycle. Hence the business cycle is an important determinant of profit margins. Furthermore, markups also depend on labor’s bargaining power (see Kalecki, 1954). Since higher unemployment is likely to decrease both labor’s bargaining power and the substitutability of employment by wages, unemployment constitutes a significant determinant of markups. In particular, markups are a positive function of the unemployment rate. And in fact this is what the more recent literature on the subject concludes (Page 3):

“I begin with three well-known explanations of labor share or its inverse. The overhead labor-wages lag hypothesis long identified with Sherman (1972, 1997) makes labor share a function of capacity utilization. The depletion of the reserve army theory hypothesis closely identified with Boddy and Crotty (1975) makes labor share a function of unemployment. The markup theories of Goldstein (1986, 1996) make the inverse of labor share a function of unemployment and capacity utilization. Since Goldstein’s views on the impact of unemployment are along the lines of Boddy and Crotty, it is his theory on the impact of capacity utilization that is of concern here. I begin with Boddy and Crotty on the role of unemployment and then turn to the contributions of Goldstein and Sherman on the role of capacity utilization.

Unemployment and the Strength of Labor

Boddy and Crotty focused on the increase in labor share in the second part of the expansion as the outcome of the rising strength of labor. Declining rates of unemployment increase labor share by increasing product real wages for given levels of labor productivity. According to Boddy and Crotty the depletion of the reserve army can also directly affect labor productivity. Although Boddy and Crotty (1975) carried out the analysis in the Burns Mitchell NBER cyclical stages framework and not with econometrics, we argued—presciently for my purposes in the present paper– that the confidence of labor would depend both on the level of unemployment and on the change of unemployment. Most workers are not directly affected by bouts of unemployment. Their confidence should be high when the rate of unemployment is low but confidence should also be affected positively if the rate of unemployment is decreasing. Based on the above arguments, I assume that the change in labor share depends on both the rate of change of unemployment and its level. It is crucial to understand the implications of the inclusion of the level of unemployment as a determinant of the change in labor share. Suppose that the rate of unemployment is extremely low but unchanging. In the absence of the level of unemployment the prediction would be that labor share would remain constant. With the inclusion of the level of unemployment the prediction becomes that labor share would continue to rise.”

http://www.peri.umass.edu/fileadmin/pdf/conference_papers/crotty/Boddy_Crotty.pdf

And should there be any doubt whether unemployment causes labor share, or labor share causes unemployment, it’s a relatively simple exercise, given an econometric software package, to confirm that the unemployment rate Granger Causes labor share of factor income, but labor share of factor income does not Granger Cause unemployment.

(1938): ”The Determinants of the Distribution of National Income”, Econometrica, 6, 97-112.

(1954): Theory of Economic Dynamics, George Allen and Unwin, London.

The literature on price determination shows that firms’ markups depend on factors like industry concentration, collusion, demand elasticity, and the potential entry of other firms into a market. Most changes in these variables are uncorrelated across industries. Nonetheless, they are simultaneously affected by the business cycle. Hence the business cycle is an important determinant of profit margins. Furthermore, markups also depend on labor’s bargaining power (see Kalecki, 1954). Since higher unemployment is likely to decrease both labor’s bargaining power and the substitutability of employment by wages, unemployment constitutes a significant determinant of markups. In particular, markups are a positive function of the unemployment rate. And in fact this is what the more recent literature on the subject concludes (Page 3):

“I begin with three well-known explanations of labor share or its inverse. The overhead labor-wages lag hypothesis long identified with Sherman (1972, 1997) makes labor share a function of capacity utilization. The depletion of the reserve army theory hypothesis closely identified with Boddy and Crotty (1975) makes labor share a function of unemployment. The markup theories of Goldstein (1986, 1996) make the inverse of labor share a function of unemployment and capacity utilization. Since Goldstein’s views on the impact of unemployment are along the lines of Boddy and Crotty, it is his theory on the impact of capacity utilization that is of concern here. I begin with Boddy and Crotty on the role of unemployment and then turn to the contributions of Goldstein and Sherman on the role of capacity utilization.

Unemployment and the Strength of Labor

Boddy and Crotty focused on the increase in labor share in the second part of the expansion as the outcome of the rising strength of labor. Declining rates of unemployment increase labor share by increasing product real wages for given levels of labor productivity. According to Boddy and Crotty the depletion of the reserve army can also directly affect labor productivity. Although Boddy and Crotty (1975) carried out the analysis in the Burns Mitchell NBER cyclical stages framework and not with econometrics, we argued—presciently for my purposes in the present paper– that the confidence of labor would depend both on the level of unemployment and on the change of unemployment. Most workers are not directly affected by bouts of unemployment. Their confidence should be high when the rate of unemployment is low but confidence should also be affected positively if the rate of unemployment is decreasing. Based on the above arguments, I assume that the change in labor share depends on both the rate of change of unemployment and its level. It is crucial to understand the implications of the inclusion of the level of unemployment as a determinant of the change in labor share. Suppose that the rate of unemployment is extremely low but unchanging. In the absence of the level of unemployment the prediction would be that labor share would remain constant. With the inclusion of the level of unemployment the prediction becomes that labor share would continue to rise.”

http://www.peri.umass.edu/fileadmin/pdf/conference_papers/crotty/Boddy_Crotty.pdf

And should there be any doubt whether unemployment causes labor share, or labor share causes unemployment, it’s a relatively simple exercise, given an econometric software package, to confirm that the unemployment rate Granger Causes labor share of factor income, but labor share of factor income does not Granger Cause unemployment.

Call in The Texas grangers

Paine said in reply to Mark A. Sadowski...

An important distinction kalecki makes somewhere

Originally in polish of course

Mark up v net margin

The price slashing triggered by a realization crisis

Versus holding ones price

Must be distinguished

from the squeeze on net margins

as fixed costs are spread

Over a smaller then anticipated and or required

revenue aggregate

Originally in polish of course

Mark up v net margin

The price slashing triggered by a realization crisis

Versus holding ones price

Must be distinguished

from the squeeze on net margins

as fixed costs are spread

Over a smaller then anticipated and or required

revenue aggregate

Mark A. Sadowski said in reply to bakho...

So the question then becomes, what determines unemployment?

Well the level of aggregate demand of course. By definition:

1) Aggregate demand (AD) is the total demand for final goods and services in the economy at a given time and price level.

2) Aggregate supply (AS) is the total amount of goods and services that firms are willing to sell at a given price level in an economy.

The AD-AS model is almost always represented graphically:

http://upload.wikimedia.org/wikipedia/commons/2/25/AS_%2B_AD_graph.svg

The intersection of AD and AS determines the price level and the level of real output. The level of employment is a function of the level of output. (Keynes repeatedly refers to the relationship between output and employment in The General Theory.) And the unemployment rate is simply the precentage of the labor force that is not employed.

Thus, as Adair Turner recently pointed out in his speech on Overt Monetary Finance (OMF) (see Slide 21):

http://ineteconomics.org/sites/inet.civicactions.net/files/Adair%20Lord%20Turner-%202013%20INET%20HONG%20KONG%20Keynote%20Slides.pdf

1) Fiscal and monetary policy determine AD which is equal to nominal GDP or NGDP.

2) And AD determines prices and real output.

Well the level of aggregate demand of course. By definition:

1) Aggregate demand (AD) is the total demand for final goods and services in the economy at a given time and price level.

2) Aggregate supply (AS) is the total amount of goods and services that firms are willing to sell at a given price level in an economy.

The AD-AS model is almost always represented graphically:

http://upload.wikimedia.org/wikipedia/commons/2/25/AS_%2B_AD_graph.svg

{kind=link}

The intersection of AD and AS determines the price level and the level of real output. The level of employment is a function of the level of output. (Keynes repeatedly refers to the relationship between output and employment in The General Theory.) And the unemployment rate is simply the precentage of the labor force that is not employed.

Thus, as Adair Turner recently pointed out in his speech on Overt Monetary Finance (OMF) (see Slide 21):

http://ineteconomics.org/sites/inet.civicactions.net/files/Adair%20Lord%20Turner-%202013%20INET%20HONG%20KONG%20Keynote%20Slides.pdf

1) Fiscal and monetary policy determine AD which is equal to nominal GDP or NGDP.

2) And AD determines prices and real output.

bakho said in reply to Mark A. Sadowski...

Yes and fiscal policy could increase demand directly. Monetary policy cannot increase demand (absent negative interest rates (which would really equal fiscal policy)) because the low demand has raised risk premiums above rate of return available at zero interest rate. Either investment would need to be subsidized or demand stimulated to reduce investment risk. The easiest and cheapest way is to simulate demand, which decreases investment risk and pushes the economy away from the ZLB where monetary policy can get traction.

Monetary policy, no matter how good, cannot compensate for bad or inadequate fiscal and regulatory policy.

Monetary policy, no matter how good, cannot compensate for bad or inadequate fiscal and regulatory policy.

Mark A. Sadowski said in reply to bakho...

The Traditional Interest Rate Channel is only one of the nine channels of the Monetary Transmission Mechanism (MTM) as enumerated by Frederic Mishkin.

The following paper by Mishkin gives an overview of the MTM:

http://myweb.fcu.edu.tw/~T82106/MTP/Ch26-supplement.pdf

You might find the following table, found in the author's best selling intermediate monetary economics textbook useful:

http://www.econbrowser.com/archives/2008/01/mishkin1.jpg

To understand what's been driving the recovery since 2009Q2 it might be useful to look at real GDP (RGDP):

http://www.bea.gov/iTable/iTableHtml.cfm?reqid=9&step=3&isuri=1&910=X&911=0&903=6&904=2009&905=2013&906=Q

Over the past 16 quarters RGDP has increased by $1291.8 billion in 2009 dollars at an annual rate. Net exports have subtracted $91.2 billion and government consumption and investment has subtracted $191.6 billion. Thus the other components of RGDP have grown by $1574.6 billion. Investment has contributed $594.1 billion (37.7%), consumption $567.8 billion (36.1%), durable goods $321.6 billion (20.4%) and residential investment $109.2 billion (6.9%). (It doesn't add up to 100% because of the residual.)

There are some immediate takeaways from this breakdown.

1) Given that there are only two ways policy makers can impact aggregate demand, fiscal and monetary policy, and that government consumption and investment has been an enourmous drag on the recovery, it's safe to say whatever recovery we have is due entirely to monetary policy.

2) Since net exports have been a net drag it's also safe to say that the Exchange Rate Channel has not contributed to the recovery. This is not surprising given the dollar's relative strength compared to many of the U.S.' trading partners, as well as relatively weak demand abroad.

3) Non-residential investment has contributed substantially to the recovery. But since so many channels impact it, it's difficult to say without further analysis what the relative contribution of each of the channels is.

4) Consumption's contribution to the recovery is also substantial, and this implies that the Wealth Effects Channel is probably the most important source of the recovery so far. This should not be too surprising in that household sector net worth has risen from about $48.7 trillion in 2009Q1 to $70.3 trillion in 2013Q1 according to the Federal Reserve Flow of Funds:

http://www.federalreserve.gov/releases/z1/

5) Durable goods have also contributed strongly to the recovery and this implies that the Traditional Interest Rate Effects Channel and the Household Liquidity Effects Channels have been important. (Note that the Household Liquidity Effects Channel is also asset price driven.)

6) Residential Investment so far has contributed relatively little, which tends to speak against the Bank Lending Channel's importance during this recovery, since mortgage lending accounts for three quarters of household sector debt. This shouldn't be too surprising given that the household sector's outstanding mortgage balance has shrunk by $1,083.1 billion since 2009Q2.

The following paper by Mishkin gives an overview of the MTM:

http://myweb.fcu.edu.tw/~T82106/MTP/Ch26-supplement.pdf

You might find the following table, found in the author's best selling intermediate monetary economics textbook useful:

http://www.econbrowser.com/archives/2008/01/mishkin1.jpg

{kind=link}

To understand what's been driving the recovery since 2009Q2 it might be useful to look at real GDP (RGDP):

http://www.bea.gov/iTable/iTableHtml.cfm?reqid=9&step=3&isuri=1&910=X&911=0&903=6&904=2009&905=2013&906=Q

Over the past 16 quarters RGDP has increased by $1291.8 billion in 2009 dollars at an annual rate. Net exports have subtracted $91.2 billion and government consumption and investment has subtracted $191.6 billion. Thus the other components of RGDP have grown by $1574.6 billion. Investment has contributed $594.1 billion (37.7%), consumption $567.8 billion (36.1%), durable goods $321.6 billion (20.4%) and residential investment $109.2 billion (6.9%). (It doesn't add up to 100% because of the residual.)

There are some immediate takeaways from this breakdown.

1) Given that there are only two ways policy makers can impact aggregate demand, fiscal and monetary policy, and that government consumption and investment has been an enourmous drag on the recovery, it's safe to say whatever recovery we have is due entirely to monetary policy.

2) Since net exports have been a net drag it's also safe to say that the Exchange Rate Channel has not contributed to the recovery. This is not surprising given the dollar's relative strength compared to many of the U.S.' trading partners, as well as relatively weak demand abroad.

3) Non-residential investment has contributed substantially to the recovery. But since so many channels impact it, it's difficult to say without further analysis what the relative contribution of each of the channels is.

4) Consumption's contribution to the recovery is also substantial, and this implies that the Wealth Effects Channel is probably the most important source of the recovery so far. This should not be too surprising in that household sector net worth has risen from about $48.7 trillion in 2009Q1 to $70.3 trillion in 2013Q1 according to the Federal Reserve Flow of Funds:

http://www.federalreserve.gov/releases/z1/

5) Durable goods have also contributed strongly to the recovery and this implies that the Traditional Interest Rate Effects Channel and the Household Liquidity Effects Channels have been important. (Note that the Household Liquidity Effects Channel is also asset price driven.)

6) Residential Investment so far has contributed relatively little, which tends to speak against the Bank Lending Channel's importance during this recovery, since mortgage lending accounts for three quarters of household sector debt. This shouldn't be too surprising given that the household sector's outstanding mortgage balance has shrunk by $1,083.1 billion since 2009Q2.

Mark A. Sadowski said in reply to bakho...

Compensation of Employees reached its peak share (67.7%) of National Income in 1980:

http://research.stlouisfed.org/fred2/graph/?graph_id=132281&category_id=0

And that happens to be the peak year for inflation as well. Coincidence?

The labor share of income during the age of disinflation has declined pretty much everywhere in the advanced world.

Peak Core CPI Rate*, Peak and Recent Labor Share of Income (Total Economy) (*Except Portugal)

Nation------CPI-Year-- Peak-Year-Recent-Year-Change

US----------12.4-1980-69.6---1980-63.7---2010--5.9

Japan-------20.2-1974-72.5---1977-56.6---2009-14.9

Germany------6.8-1974-76.3---1974-68.5---2011--7.8

UK----------22.1-1975-75.6---1975-71.3---2010--4.3

France------12.7-1980-79.2---1981-68.4---2010-10.8

Italy-------22.3-1980-83.4---1971-68.1---2010-15.3

Spain-------26.4-1977-76.4---1977-59.9---2011-16.5

Canada------11.1-1980-68.1---1971-59.8---2008--8.3

Australia---12.8-1977-75.5---1975-61.3---2006-14.2

Neth.-------10.5-1975-77.1---1975-68.5---2010--8.6

Sweden------12.5-1980-77.9---1978-63.3---2011-14.6

Switzerland--8.9-1974-67.5---2002-65.9---2010--1.6

Austria-----11.1-1981-98.5---1978-66.3---2011-32.2

Norway------12.2-1981-73.7---1977-55.4---2011-18.3

Portugal*---33.1-1977-83.9---1975-66.4---2010-17.5

Denmark-----10.6-1978-73.7---1980-69.5---2011--4.2

Finland-----17.5-1975-76.9---1991-66.1---2011-10.8

Ireland-----21.2-1981-79.3---1980-60.9---2010-18.4

New Zeal.—--17.2-1982-60.7---1975-49.0---2006-11.7

The international labor share data comes from the OECD and is not consistent with BEA data:

http://stats.oecd.org/Index.aspx?queryname=345&querytype=view

Select *Total Economy*.

Although there are many reasons for the increase in inequality that we have seen in the US and in other parts of the world (regressive taxation, weaker unions, lower minimum wages, globalization, Skills-Based-Technological-Change (SBTC) etc.) the leading hypothesis for why there has been such large scale declines in the labor share of factor income is disinflation (i.e. tight monetary policy).

Disinflation during the eighties and the nineties was accompanied by a significant rise in the profit share of national income in most OECD countries or, equivalently, by a reduction in the labor share. This suggests that changes in the rate of inflation are non-neutral with respect to the distribution of factor income. The consequences of inflation upon inequality thus may largely be the indirect result of the effects of inflation upon factor shares. The mechanism by which this comes about is fairly simple. Accelerating inflation is correlated to falling unemployment rates, falling unemployment rates lead to greater labor bargaining power, and greater labor bargaining power is correlated with lower markups. Furthermore, higher inflation rates create greater price dispersion leading to greater competition among producers to limit markups. This hypothesis was tested with a panel of 15 OECD countries over the period from 1960 to 2000 and a robust positive relationship between inflation and the labor share was obtained:

Inflation and Factor Shares

Francisco Alcalá and F. Israel Sanchoy

August 2000

Abstract: “We use results from the literature on the determinants of price-cost margins to derive an equation relating labor’s share of national income to the inflation rate (as well as to the output gap, the unemployment rate and the capital stock per worker). The equation is tested with a panel of 15 OECD countries. We obtain a robust positive relationship between inflation and the labor share. Our results suggest that disinflation is not distributively neutral, provide empirical support for the distinct concern about price stability shown by trade unions and employers’ organizations, and help explaining the negative impact of inflation on growth.”

http://pareto.uab.es/wp/2000/46000.pdf

http://research.stlouisfed.org/fred2/graph/?graph_id=132281&category_id=0

And that happens to be the peak year for inflation as well. Coincidence?

The labor share of income during the age of disinflation has declined pretty much everywhere in the advanced world.

Peak Core CPI Rate*, Peak and Recent Labor Share of Income (Total Economy) (*Except Portugal)

Nation------CPI-Year-- Peak-Year-Recent-Year-Change

US----------12.4-1980-69.6---1980-63.7---2010--5.9

Japan-------20.2-1974-72.5---1977-56.6---2009-14.9

Germany------6.8-1974-76.3---1974-68.5---2011--7.8

UK----------22.1-1975-75.6---1975-71.3---2010--4.3

France------12.7-1980-79.2---1981-68.4---2010-10.8

Italy-------22.3-1980-83.4---1971-68.1---2010-15.3

Spain-------26.4-1977-76.4---1977-59.9---2011-16.5

Canada------11.1-1980-68.1---1971-59.8---2008--8.3

Australia---12.8-1977-75.5---1975-61.3---2006-14.2

Neth.-------10.5-1975-77.1---1975-68.5---2010--8.6

Sweden------12.5-1980-77.9---1978-63.3---2011-14.6

Switzerland--8.9-1974-67.5---2002-65.9---2010--1.6

Austria-----11.1-1981-98.5---1978-66.3---2011-32.2

Norway------12.2-1981-73.7---1977-55.4---2011-18.3

Portugal*---33.1-1977-83.9---1975-66.4---2010-17.5

Denmark-----10.6-1978-73.7---1980-69.5---2011--4.2

Finland-----17.5-1975-76.9---1991-66.1---2011-10.8

Ireland-----21.2-1981-79.3---1980-60.9---2010-18.4

New Zeal.—--17.2-1982-60.7---1975-49.0---2006-11.7

The international labor share data comes from the OECD and is not consistent with BEA data:

http://stats.oecd.org/Index.aspx?queryname=345&querytype=view

Select *Total Economy*.

Although there are many reasons for the increase in inequality that we have seen in the US and in other parts of the world (regressive taxation, weaker unions, lower minimum wages, globalization, Skills-Based-Technological-Change (SBTC) etc.) the leading hypothesis for why there has been such large scale declines in the labor share of factor income is disinflation (i.e. tight monetary policy).

Disinflation during the eighties and the nineties was accompanied by a significant rise in the profit share of national income in most OECD countries or, equivalently, by a reduction in the labor share. This suggests that changes in the rate of inflation are non-neutral with respect to the distribution of factor income. The consequences of inflation upon inequality thus may largely be the indirect result of the effects of inflation upon factor shares. The mechanism by which this comes about is fairly simple. Accelerating inflation is correlated to falling unemployment rates, falling unemployment rates lead to greater labor bargaining power, and greater labor bargaining power is correlated with lower markups. Furthermore, higher inflation rates create greater price dispersion leading to greater competition among producers to limit markups. This hypothesis was tested with a panel of 15 OECD countries over the period from 1960 to 2000 and a robust positive relationship between inflation and the labor share was obtained:

Inflation and Factor Shares

Francisco Alcalá and F. Israel Sanchoy

August 2000

Abstract: “We use results from the literature on the determinants of price-cost margins to derive an equation relating labor’s share of national income to the inflation rate (as well as to the output gap, the unemployment rate and the capital stock per worker). The equation is tested with a panel of 15 OECD countries. We obtain a robust positive relationship between inflation and the labor share. Our results suggest that disinflation is not distributively neutral, provide empirical support for the distinct concern about price stability shown by trade unions and employers’ organizations, and help explaining the negative impact of inflation on growth.”

http://pareto.uab.es/wp/2000/46000.pdf

Paine said in reply to Mark A. Sadowski...

Accelerating output price change

Is always correlated to falling unemployment ?

Is always correlated to falling unemployment ?

What marvels of torture by lag and lead might yield this iron law my friend ?

Mark A. Sadowski said in reply to Paine ...

Did I use the word "always"?

The Phillips Curve slopes downward, no?

The Phillips Curve slopes downward, no?

paine said in reply to Mark A. Sadowski...

no u didn't

but if not then when not or when if its easier to include then exclude

I think you realize you left out

a few

contextualizing links

in your chain

I refuse to think about

the Phillips screw wages magic equations differential or otherwise

the conception is pure mind trap

but if not then when not or when if its easier to include then exclude

I think you realize you left out

a few

contextualizing links

in your chain

I refuse to think about

the Phillips screw wages magic equations differential or otherwise

the conception is pure mind trap

samuel said...

No one expects the ... Zero Lower Bound!

But seriously, we need to start paying people more than what they made 10 years ago.

But seriously, we need to start paying people more than what they made 10 years ago.

reason said in reply to samuel...

Easy - institute (an initially small) citizens basic income. No other changes necessary (but you could increase some taxes on the rich to help pay for it).

paine said in reply to reason...

I agree we need to use the tax or borrow to transfer system

to tighten domestic job markets and mobilize domestic productive factors to the max

but only if you use

the dollar forex aggressively

to keep trade in balance

since a plunging dollar

means relative prices on imports must rise

the forex fiddling

among other effects

jumps job class cost of living

and to this extent

tight job market's

net impact

on real wage rates

is partially off set

to tighten domestic job markets and mobilize domestic productive factors to the max

but only if you use

the dollar forex aggressively

to keep trade in balance

since a plunging dollar

means relative prices on imports must rise

the forex fiddling

among other effects

jumps job class cost of living

and to this extent

tight job market's

net impact

on real wage rates

is partially off set

reason said in reply to paine ...

If you print enough money you kill the $ as a reserve currency. Even pigs eat their fill eventually.

What suggests to u the American job class over the longest haul

benefits by hosting the global reserve currency

benefits by hosting the global reserve currency

pgl said...

Metzler was writing sensible things about QE when Japan went through this mess. Ah but now it is the US with a Democrat as President and Metzler is with the AEI. So now it is all different - somehow.

ilsm said in reply to pgl...

Reprised Upton Sinclair: “It is difficult to get a man to understand something, when his salary depends on his not understanding it.” Upton Sinclair

paine said in reply to pgl...

his absurdly reactionary

shadow fomc bull shit

glares out at us

from his record

he has a long history

trailing back decades

of reactionary anti job class macro Rx

shadow fomc bull shit

glares out at us

from his record

he has a long history

trailing back decades

of reactionary anti job class macro Rx

paine said in reply to paine ...

when meltzers politics crash

into his understanding of money markets etc

his politics win every time

into his understanding of money markets etc

his politics win every time

The PolyCapitalist said...

Generating inflation would be easy if people would stop believing in the Zero Lower Bound Myth:

http://www.polycapitalist.com/2013/05/krugman-perpetuates-myth-of-zero-lower.html

http://www.polycapitalist.com/2013/05/krugman-perpetuates-myth-of-zero-lower.html

reason said in reply to The PolyCapitalist...

What?

Oh come on, what proportion of the population pays attention to Krugman, or to you for that matter. You're nuts, most people don't theorise about these things.

Besides your linked post talks about cutting nominal interest rates, not "creating inflation".

Oh come on, what proportion of the population pays attention to Krugman, or to you for that matter. You're nuts, most people don't theorise about these things.

Besides your linked post talks about cutting nominal interest rates, not "creating inflation".

Main Street Muse said...

I am not an economist and I have not read any economic history recently. When was the US in the middle of an inflationary hot mess? Starting in the Nixon era and ending with the Reagan era, right? And while people want to blame monetary policy, there were other things going on - like the rise of OPEC, etc. I remember when "gas was running out." I was a wee one then, but wasn't there gas rationing? You could by gas on particular days only? I could be wrong...

When were the other major inflationary eras in US history?

And, as I understand it, no one outside of the C-suites and on Wall Street has gotten a raise since them. Gas has gone up quite a lot, but wages have remained stagnant. And inflation has remained low. And we keep obsessing about inflation?

When were the other major inflationary eras in US history?

And, as I understand it, no one outside of the C-suites and on Wall Street has gotten a raise since them. Gas has gone up quite a lot, but wages have remained stagnant. And inflation has remained low. And we keep obsessing about inflation?

Peter K. said in reply to Main Street Muse...

The 1970s were not that bad. Organized labor was strong enough to negotiate wage increases in their contracts which helped develop a wage-price spiral. Unfortunately they're not powerful enough today to repeat that.

Main Street Muse said in reply to Peter K....

They were very bad if you wanted to get a mortgage (interest rates being above 15%, I believe.)

Mark A. Sadowski said in reply to Main Street Muse...

Here’s a relatively simple way to frame this.

The following link is to a dynamic AD-AS diagram, and which can be found in “Modern Principles: Macroeconomics” by Tyler Cowen and Alex Tabarrok:

https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEg5NY6bn3oZEPheIRUWXkyV3Ee-aQQ-K-Oi3cA4quTxS3XntC5IztnqqqahbFCAxB9OcU5CcaBcWmdsw47gbTYAApvJ8SlqYY8cmZl0t6KgexabOuqGKDhZHER4xj0cLA3Q0hh0-34-u_U/s1600-h/Tabarrok-Cowen+ADAS.JPG

You’ll note that the rate of change in the aggregate demand (AD) curve is equal to the sum of the inflation rate and the rate of change in real GDP (RGDP), and so is precisely equal to the rate of change in nominal GDP (NGDP). The rate of change in NGDP is determined by both fiscal and monetary policy in the short run but in the long run the rate of change in NGDP is determined solely by monetary policy.

Note also the short run aggregate supply (SRAS/AS) curve and the Solow growth curve. The Solow growth curve is essentially the long run AS curve (LRAS). In the short run wages and prices are sticky causing the SRAS curve to be upwardly sloped. In the long run money is neutral and wages and prices are flexible so the Solow growth curve is vertical. Thus shifts in AD influence the rate of growth of RGDP in the short run, but not in the long run.

Similarly, shifts in AS influence the inflation rate in the short run, but in the long run the inflation rate is determined solely by AD (i.e. monetary policy).

The following link is to a dynamic AD-AS diagram, and which can be found in “Modern Principles: Macroeconomics” by Tyler Cowen and Alex Tabarrok:

https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEg5NY6bn3oZEPheIRUWXkyV3Ee-aQQ-K-Oi3cA4quTxS3XntC5IztnqqqahbFCAxB9OcU5CcaBcWmdsw47gbTYAApvJ8SlqYY8cmZl0t6KgexabOuqGKDhZHER4xj0cLA3Q0hh0-34-u_U/s1600-h/Tabarrok-Cowen+ADAS.JPG

{kind=link}

You’ll note that the rate of change in the aggregate demand (AD) curve is equal to the sum of the inflation rate and the rate of change in real GDP (RGDP), and so is precisely equal to the rate of change in nominal GDP (NGDP). The rate of change in NGDP is determined by both fiscal and monetary policy in the short run but in the long run the rate of change in NGDP is determined solely by monetary policy.

Note also the short run aggregate supply (SRAS/AS) curve and the Solow growth curve. The Solow growth curve is essentially the long run AS curve (LRAS). In the short run wages and prices are sticky causing the SRAS curve to be upwardly sloped. In the long run money is neutral and wages and prices are flexible so the Solow growth curve is vertical. Thus shifts in AD influence the rate of growth of RGDP in the short run, but not in the long run.

Similarly, shifts in AS influence the inflation rate in the short run, but in the long run the inflation rate is determined solely by AD (i.e. monetary policy).

Soley by monetary policy

In the model only or also in reality ?

In the model only or also in reality ?

The notion of long run is extrapolative

Not in any sense an estimate of future reality

As Lerner sez

In the long run we are in another short run

The sinister smuggling in of neutrality conditions and the like

Make these models into a hustle

Not in any sense an estimate of future reality

As Lerner sez

In the long run we are in another short run

The sinister smuggling in of neutrality conditions and the like

Make these models into a hustle

Mark A. Sadowski said in reply to Paine ...

Fiscal stimulus requires increases in the cyclically adjusted budget balance. This cannot be done indefinitely.

paine said in reply to Mark A. Sadowski...

ahh so you fall into the nominal rigidity trap

the nominal obligations of the state with a limitless money mine are paper shackles

btw

we need a better term for debt management

then financial repression

don't you agree ?

something positive like

fully managed carry costs

you ngdp types oughta see

your magic target

onc u break fre of this silly fear

of some sort of inertial moment

in product price and wage inflation

once you get the hang of forward guidance

talk of ngdp slope change

is just the gimmick

for paving over

a slug of financial repression

the nominal obligations of the state with a limitless money mine are paper shackles

btw

we need a better term for debt management

then financial repression

don't you agree ?

something positive like

fully managed carry costs

you ngdp types oughta see

your magic target

onc u break fre of this silly fear

of some sort of inertial moment

in product price and wage inflation

once you get the hang of forward guidance

talk of ngdp slope change

is just the gimmick

for paving over

a slug of financial repression

paine said in reply to paine ...

to be perfectly fair

why would one require constantly increasing primary deficits

given the other macro levers

at no point would I dispense with any of them

fiscal first transfer first FFTF

is a job class welfare first

policy maxim

for obvious reasons I way too often reiterate

but the wind hollows out here in left field

and I shout to keep my head warm

why would one require constantly increasing primary deficits

given the other macro levers

at no point would I dispense with any of them

fiscal first transfer first FFTF

is a job class welfare first

policy maxim

for obvious reasons I way too often reiterate

but the wind hollows out here in left field

and I shout to keep my head warm

Mark A. Sadowski said in reply to Paine ...

It's actually a pretty good textbook and the diagram is enormously useful (it's far less confusing to students than the usual ones).

Despite the fact Tyler Cowen has implied that I do not share his "mood affilitation" he has made posts out of my comments, so I now choose to be polite in return:

http://marginalrevolution.com/marginalrevolution/2013/05/from-the-comments-15.html

Despite the fact Tyler Cowen has implied that I do not share his "mood affilitation" he has made posts out of my comments, so I now choose to be polite in return:

http://marginalrevolution.com/marginalrevolution/2013/05/from-the-comments-15.html

paine said in reply to Mark A. Sadowski...

very wise of you

play it suave and diplomatical

you are nothing

if not discretely sadistic

in fact

you're nothing but

discretely sadistic

play it suave and diplomatical

you are nothing

if not discretely sadistic

in fact

you're nothing but

discretely sadistic

paine said in reply to paine ...

btw

these stars will gladly exploit your

boundless diligence

while retaining the there gathered habitual

readership

they the ever vigilant axe to grind

hosters with the toasters

can burn you off the site's face

at any time

again get your own blog

make the mountain come to Mo-ham-ski

these stars will gladly exploit your

boundless diligence

while retaining the there gathered habitual

readership

they the ever vigilant axe to grind

hosters with the toasters

can burn you off the site's face

at any time

again get your own blog

make the mountain come to Mo-ham-ski

Mark A. Sadowski said in reply to Main Street Muse...

Here's a century of year on year CPI and PPI inflation rates. Enjoy!

http://research.stlouisfed.org/fred2/graph/?graph_id=133017&category_id=0

http://research.stlouisfed.org/fred2/graph/?graph_id=133017&category_id=0

don said in reply to Mark A. Sadowski...

Thanks Mark. Can you show us one of inflation against the monetary base that goes back before 1929?

Mark A. Sadowski said in reply to don...

Here's the same graph with the monetary base added. Fred only has monetary base data back to 1918:

http://research.stlouisfed.org/fred2/graph/?graph_id=133048&category_id=0

If the Fed is targeting inflation we expect the correlation to be negative, which over the 95 years of data, it frequently is.

http://research.stlouisfed.org/fred2/graph/?graph_id=133048&category_id=0

If the Fed is targeting inflation we expect the correlation to be negative, which over the 95 years of data, it frequently is.

BigBozat said in reply to Main Street Muse...

Main Street Muse asked:

"When were the other major inflationary eras in US history?"

Depends on how & what is measured (some statistical series don't go back all that far)...

Short version:

2 waves post-WW II, both relatively brief... One immediately after the war (removal of price controls) & second @ onset of Korean War @ late 1950...

WW II (late '41 ~ mid-late '43)

WW I & aftermath (1916 ~ 1920)

Standard series only goes back to 1913...

Before then:

Civil War... 'tho we subsequently went through an extended deflationary period after the war in order to bring bring the economy back onto a gold standard.

Prior to that: the War of 1812, and the Revolutionary War (think scrip).

Using wholesale commodity prices as surrogate for inflation measure see, e.g.: http://fraser.stlouisfed.org/docs/publications/1943chart_busibooms.pdf

"When were the other major inflationary eras in US history?"

Depends on how & what is measured (some statistical series don't go back all that far)...

Short version:

2 waves post-WW II, both relatively brief... One immediately after the war (removal of price controls) & second @ onset of Korean War @ late 1950...

WW II (late '41 ~ mid-late '43)

WW I & aftermath (1916 ~ 1920)

Standard series only goes back to 1913...

Before then:

Civil War... 'tho we subsequently went through an extended deflationary period after the war in order to bring bring the economy back onto a gold standard.

Prior to that: the War of 1812, and the Revolutionary War (think scrip).

Using wholesale commodity prices as surrogate for inflation measure see, e.g.: http://fraser.stlouisfed.org/docs/publications/1943chart_busibooms.pdf

The long return to gold post 1865

Is quite a sage

A trail of tears in fact

Is quite a sage

A trail of tears in fact

I put doesn't like the word saga

bakho said in reply to Main Street Muse...

Yes. Oil demand was much greater than supply. Carter energy policy fixed this so that oil demand dropped by 22 percent from its peak in 1978 and 1983.

Monetarists claim victory and lionize Volcker, but Volcker would have been unsuccessful without Carter energy policy.

Monetarists claim victory and lionize Volcker, but Volcker would have been unsuccessful without Carter energy policy.

Charlie Baker said in reply to bakho...

I very much agree with this. The Carter energy policy reduced petroleum imports sharply, and were a major aid to recovery in the '80s.

The total amount of US imports did not surpass its 1977-79 peak until 1993.

http://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=pet&s=mcrimus1&f=a

Even today, we are a more fuel efficient country than we were in the '70s, so much that oil price shocks do not have the same impact now as then.

The total amount of US imports did not surpass its 1977-79 peak until 1993.

http://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=pet&s=mcrimus1&f=a

Even today, we are a more fuel efficient country than we were in the '70s, so much that oil price shocks do not have the same impact now as then.

Paine said in reply to Charlie Baker...

The history in numbers

Of the energy share in GDP must be at anne's finger tips

Of the energy share in GDP must be at anne's finger tips

But I must insist we give volcker credit

where goes the credit

also goes the blame

The horrifically un necessary butchery of the Volcker Carter Reagan double dipper

The second scoop deeper then the first by far of course

where goes the credit

also goes the blame

The horrifically un necessary butchery of the Volcker Carter Reagan double dipper

The second scoop deeper then the first by far of course

Mark A. Sadowski said in reply to Paine ...

"The history in numbers

Of the energy share in GDP must be at anne's finger tips"

Personal consumption expenditures on gasoline and other energy goods were 4.0% of personal consumption expenditures (PCE) in 2012:

http://research.stlouisfed.org/fred2/graph/?graph_id=121946&category_id=0

By comparison they were above 4.0% of PCE in 1974-85 and peaked at 5.8% of PCE in 1980-81. Given the inherently volatile nature of energy prices this of course meant consumer prices were more volatile back then.

Of the energy share in GDP must be at anne's finger tips"

Personal consumption expenditures on gasoline and other energy goods were 4.0% of personal consumption expenditures (PCE) in 2012:

http://research.stlouisfed.org/fred2/graph/?graph_id=121946&category_id=0